{kind=link}

Key Factors

-

The S&P 500 has cruised to a file excessive and is buying and selling at lofty valuations.

-

The Motley Idiot CEO urges traders to take a distinct method to investing now.

Traders in inventory markets have witnessed historic volatility in 2025 to date. After peaking in February, the S&P 500 (SNPINDEX: ^GSPC) index briefly slipped into correction territory in April. Many feared a market crash, however the S&P 500 has as an alternative staged one among its most dramatic V-shaped recoveries since and simply hit a file excessive.

The wild trip has left traders questioning whether or not the inventory market is overheated and whether or not they need to put money into shares now or stay on the sidelines. The concern is warranted. The S&P 500 is at present buying and selling at over 25 occasions earnings, and U.S. shares now account for 65% of all shares worldwide. These are traditionally excessive valuations.

The place to speculate $1,000 proper now? Our analyst staff simply revealed what they imagine are the 10 greatest shares to purchase proper now. Proceed »

But, even at these lofty market ranges, you possibly can nonetheless beat the market in the long run if you understand the place to look. The Motley Idiot CEO and co-founder, Tom Gardner, believes the important thing to beating the market now lies in trying “the place individuals aren’t trying.”

Picture supply: Getty Photographs.

The kind of shares traders can buy now

In a latest interview, Gardner shared his perspective on the present state of the market and the way traders ought to method investing. Whereas recognizing that the markets are at excessive valuations, Gardner maintains that there are nonetheless a whole bunch of fine shares you might purchase now, however they’re most likely “not probably the most well-known, actively adopted, most richly valued” shares. Gardner believes it is time to be “somewhat extra defensive” proper now and search for investments “the place others aren’t trying.”

I am saying should you’re on the lookout for good returns over the following 3-5 years that beat the market, I believe it is advisable look the place others aren’t trying now, and it is advisable search for dividend payers, extra value-oriented investing. A minimum of the place we’re in valuation now.

So, the place are you able to look to speculate now? Suppose dividends, defensive, and worth shares.

Whereas good dividend shares can generate a gentle stream of passive revenue even throughout turbulent occasions, defensive shares are sometimes recession-proof shares and an effective way to cut back your portfolio danger. Worth shares, in the meantime, commerce for a worth decrease than what their fundamentals benefit. As a rule, among the most boring companies match two or extra of those three inventory classes, and there are many such shares at present that might beat the market in the long run.

In at present’s atmosphere, three shares come to thoughts.

A 6.9%-yielding protected power dividend inventory

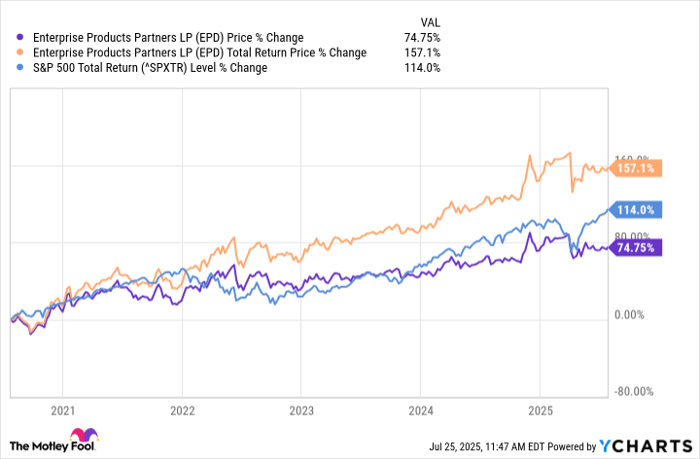

Enterprise Merchandise Companions (NYSE: EPD) is without doubt one of the largest midstream power corporations within the U.S., proudly owning over 50,000 miles of pipeline. It shops, processes, and transports pure gasoline liquids and different merchandise underneath long-term contracts in return for a payment. The enterprise is recession-proof and largely proof against the volatility in oil and gasoline costs. Furthermore, 90% of the contracts have escalation clauses to offset the results of inflation.

All these elements mixed imply that Enterprise Merchandise can generate regular, predictable money flows and pay common, rising dividends. The power large has elevated its dividend for 26 consecutive years, and the inventory yields a hefty 6.9%. With Enterprise Merchandise bringing $6 billion of the $7.6 billion in main capital initiatives on-line this yr, traders can count on to see regular development in its money flows and dividends, no matter the place the economic system or inventory markets are.

A defensive dividend development wager

Brookfield Infrastructure‘s (NYSE: BIPC)(NYSE: BIP) enterprise can also be recession-resilient, because it earns from defensive property, comparable to utilities, rail and toll roads, midstream power, and knowledge facilities. Almost 85% of Brookfield’s funds from operations (FFO) are contracted or regulated and listed to inflation. Whereas that makes its money flows predictable, common acquisitions and recycling of outdated, mature property drive money flows greater.

Over the previous 15 years, Brookfield has grown its FFO per unit by a compound annual development charge (CAGR) of 15% and its dividend by a 9% CAGR. With the corporate concentrating on over 10% FFO development and 5% to 9% annual dividend development in the long run, Brookfield Infrastructure is a good inventory to personal throughout unsure occasions. The company shares additionally yield a superb 4%.

A beaten-down Dividend King to purchase

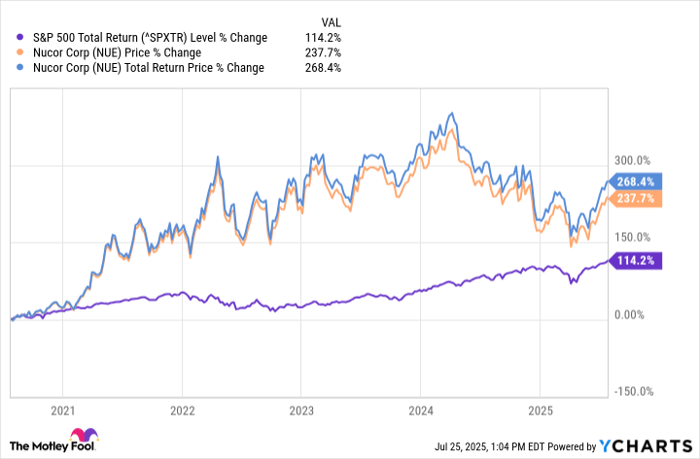

Not like Enterprise Merchandise and Brookfield Infrastructure, that are defensive shares, Nucor (NYSE: NUE) is a cyclical inventory. Nonetheless, you would be stunned to see the form of complete returns it has generated lately.

Nucor is the biggest and most diversified metal producer in North America. Whereas this exposes the corporate to commodity costs, Nucor has sailed by way of turbulent occasions primarily on account of two causes. First, it makes use of electrical arc furnaces in metal mills. They’re extra versatile, environment friendly, and cost-effective in comparison with conventional blast furnaces. Second, its mills use scrap as the important thing uncooked materials, which Nucor produces internally.

Vertical integration, a cost-efficient enterprise mannequin, and a powerful stability sheet contribute to Nucor’s standing as a Dividend King, having elevated its dividend for 52 consecutive years. With President Donald Trump imposing hefty tariffs on metal imports, Nucor could possibly be a strong turnaround story. Buying and selling at 30% off all-time highs as of this writing, Nucor is one worth plus dividend development inventory you might purchase now.

Do you have to make investments $1,000 in Enterprise Merchandise Companions proper now?

Before you purchase inventory in Enterprise Merchandise Companions, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Enterprise Merchandise Companions wasn’t one among them. The ten shares that made the lower may produce monster returns within the coming years.

Think about when Netflix made this checklist on December 17, 2004… should you invested $1,000 on the time of our advice, you’d have $636,628!* Or when Nvidia made this checklist on April 15, 2005… should you invested $1,000 on the time of our advice, you’d have $1,063,471!*

Now, it’s value noting Inventory Advisor’s complete common return is 1,041% — a market-crushing outperformance in comparison with 183% for the S&P 500. Don’t miss out on the newest high 10 checklist, accessible if you be a part of Inventory Advisor.

*Inventory Advisor returns as of July 21, 2025

Neha Chamaria has no place in any of the shares talked about. The Motley Idiot recommends Brookfield Infrastructure Companions and Enterprise Merchandise Companions. The Motley Idiot has a disclosure coverage.